How Nepalis Bypass the Cryptocurrency Ban for Remittances

May, 5 2025

May, 5 2025

Nepal Crypto Remittance Workaround Calculator

Remittance Cost Comparison

Compare traditional banking fees with crypto remittance costs for your typical transfer amount.

Traditional Banking

Transfer Amount: $200.00

Fee: $20.00

Total Cost: $220.00

Delivery Time: 3-5 days

Crypto Remittance

Transfer Amount: 0.00465 BTC

Fee: $2.00

Total Cost: $2.00

Delivery Time: 1-2 hours

Risk Assessment

Potential Legal and Financial Risks

- Legal Risk: Up to 3 years imprisonment, fines up to 3x transaction value

- Asset Risk: Confiscation of crypto assets and devices

- Fraud Risk: Scams, phishing, and unverified counterparties

- Technical Risk: Loss of private keys or malware exposure

Even though the cryptocurrency ban in Nepal is spelled out in the Foreign Exchange Regulation Act of 2019 and reinforced by the Nepal Rastra Bank (NRB), many Nepalis still turn to digital coins to send money home. The paradox-strict law versus real‑world need-has birthed a hidden ecosystem that operates under the radar of law enforcement. Below you’ll see why the ban exists, how citizens get around it, and what the future might hold.

Key Takeaways

- The ban covers trading, mining, and payments, with penalties up to three years in prison.

- Cross‑border remittances are the main driver for underground crypto use.

- Typical workarounds include offshore wallets, peer‑to‑peer apps, and VPN‑masked exchanges.

- Risks range from asset seizure to fraud, because users have no legal protection.

- A state‑run CBDC is slated for launch within two years, but it won’t legalize private crypto.

Legal Landscape: What the Government Says

In September 2021 the NRB issued a formal notice that cryptocurrency trading is illegal, punishable by up to three years imprisonment and fines up to three times the transaction value. The Electronic Transaction Act (ETA) 2063 adds cyber‑crime charges for any digital asset activity, and the government can confiscate wallets, laptops, or any device linked to the transaction.

Why Remittances Push People Toward Crypto

Nepal’s economy leans heavily on money sent home by workers abroad. Traditional remittance channels charge high fees, impose strict daily limits, and can take several days to clear. For a laborer in the Gulf or Malaysia, a $200 transfer through a bank may cost $20 in fees and arrive after 72hours. Digital coins, on the other hand, promise near‑instant settlement and lower costs-an attractive alternative when a family depends on that cash.

Underground Workarounds: How Nepalis Get Around the Ban

Because open discussion is risky, most methods are shared through private Telegram groups, Discord servers, or word‑of‑mouth. Below is a snapshot of the most common tactics.

| Method | How It Works | Key Risks |

|---|---|---|

| Offshore Exchanges | Register on platforms in India, Singapore, or the U.S.; use a VPN to hide IP; move funds via P2P transfers. | Account freeze, KYC leaks, seizure if authorities trace IP. |

| Peer‑to‑Peer (P2P) Apps | Direct crypto swaps through local groups; payment via bank transfer or cash. | Scams, no escrow protection, possible police sting. |

| Mobile Wallets with Integrated DEX | Use apps that embed decentralized exchanges; access through Android sideloading. | Malware, loss of private keys, detection by device monitoring. |

| Hardware Wallet Smuggling | Physical devices mailed abroad; funds loaded overseas then sent back as crypto. | Customs seizure, loss of device, legal penalty for possession. |

| Crypto‑Backed Remittance Services | Third‑party services that accept crypto and deliver local fiat to Nepali banks. | Regulatory crackdowns, hidden fees, limited availability. |

Who’s Behind the Curtain?

The underground network is not a single organization but a loosely connected set of actors:

- Tech‑savvy youth use their coding skills to set up VPNs, smart contracts, and private Discord bots.

- Diaspora intermediaries manage offshore wallets and act as relayers for remittance flows.

- Underground crypto exchanges operate on the dark web, offering peer‑to‑peer matching without KYC.

Risks and Penalties: What’s at Stake?

If caught, the consequences are severe. The NRB can impose a fine up to three times the transaction value, confiscate any crypto assets, and file a cyber‑crime case under the ETA. Imprisonment ranges from six months to three years, depending on the perceived severity and whether the case involves money‑laundering allegations.

Beyond legal repercussions, users face typical crypto hazards: loss of private keys, phishing attacks, and fraud from unverified counterparties. Since there is no regulatory safety net, victims have no recourse to recover lost funds.

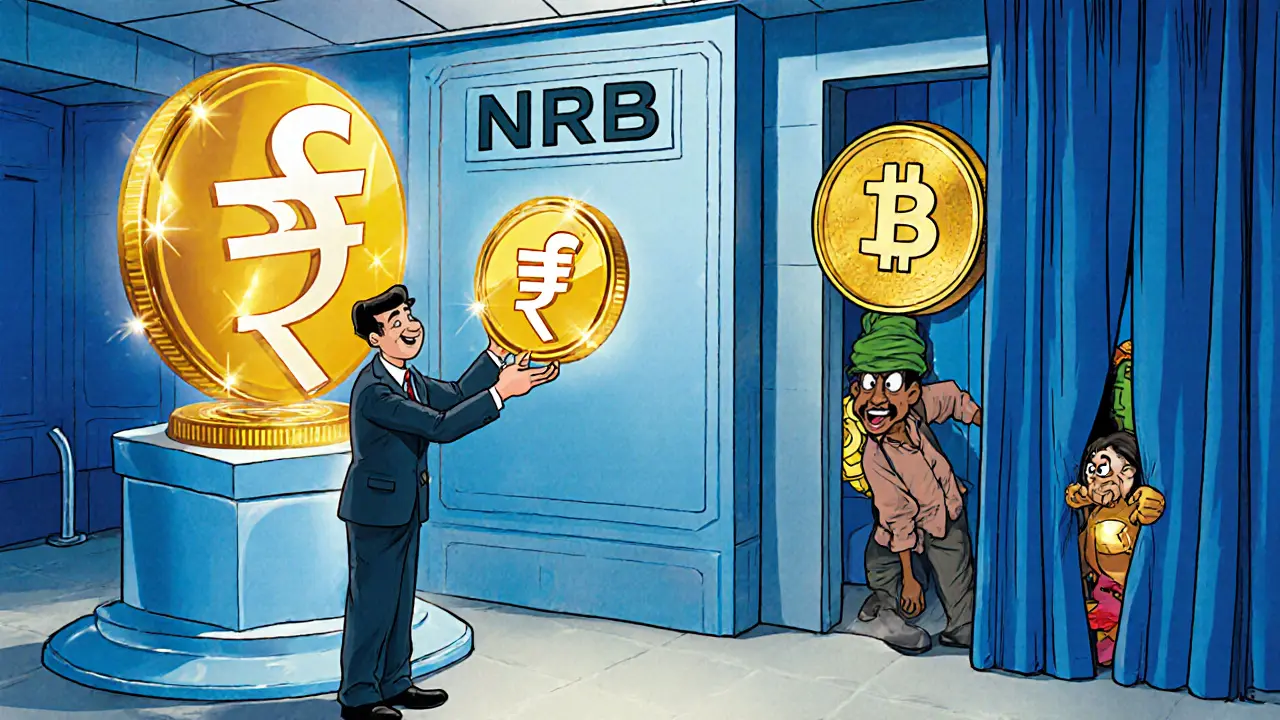

The Emerging CBDC: A Government Alternative

The Nepal Rastra Bank is developing a central bank digital currency (CBDC) expected to launch within the next two years. The CBDC will be state‑controlled, fully KYC‑compliant, and linked to the Nepalese rupee. While the government touts it as a modern way to handle payments, the CBDC does not legalize private crypto or stablecoins. It’s designed to keep digital value inside the official financial system, potentially squeezing the underground market even tighter.

Looking Ahead: Will the Ban Hold?

Pressure is building. As remittance costs stay high and the diaspora continues to look for cheaper routes, the underground crypto flow is unlikely to disappear overnight. Some analysts argue that a softened stance-perhaps permitting crypto for personal use only-could bring the activity into the light and allow for consumer protection. Others believe the upcoming CBDC will satisfy the demand for fast, low‑fee transfers, rendering private crypto less attractive.

For now, the legal reality remains unchanged: any crypto activity is illegal, and enforcement agencies are actively monitoring. Whether the ban survives the next decade will depend on how effectively the CBDC can replace the convenience that private coins currently offer.

Frequently Asked Questions

Is it illegal to own Bitcoin in Nepal?

Yes. Owning, trading, or using Bitcoin for payments violates the Foreign Exchange Regulation Act and can lead to imprisonment, fines, and asset seizure.

Why do Nepalis still use crypto despite the ban?

The main driver is cheaper, faster cross‑border remittances. Traditional channels are costly and slow, so many turn to crypto as a workaround.

What are the most common ways to bypass the ban?

People use offshore exchanges, peer‑to‑peer apps, VPN‑masked services, hardware wallet smuggling, and crypto‑backed remittance firms.

What penalties can I face if caught?

Penalties include up to three years in prison, fines up to three times the transaction amount, and confiscation of crypto assets.

Will the upcoming CBDC replace private crypto?

The CBDC aims to offer a fast, government‑backed digital payment method, but it will not legalize private cryptocurrencies or stablecoins.

Mureil Stueber

May 5, 2025 AT 10:28Just a heads‑up for anyone thinking about using crypto to send money home: the legal risks are huge, and you could lose both the cash and your freedom if you get caught. The NRB is actively monitoring offshore wallets and VPN traffic, so it’s not a game. If you do decide to go down that route, at least diversify the tools – use hardware wallets, split the amounts across multiple exchanges, and keep your private keys offline. Also, be aware that the penalties aren’t just fines; they can include up to three years in prison. A lot of people underestimate the technical skill needed to stay hidden, so brush up on strong encryption and anonymity practices. Lastly, keep an eye on the upcoming CBDC – it might make crypto workarounds even harder.

Emily Kondrk

May 12, 2025 AT 19:28Everyone’s talking about "fast" and "cheap" transfers, but have you considered the shadow network the government’s already weaving? Every VPN endpoint is a potential trap, and the NRB has a dedicated cyber‑unit sniffing packets for crypto signatures. If you think a $2 fee is worth the risk of a three‑year sentence, you’re ignoring the deeper agenda: control of the diaspora’s cash flow. The real money lies in the data they collect – your transaction patterns, your contacts, even your phone’s IMEI. Those offshore exchanges? They’re just front‑ends for state‑aligned brokers, feeding your info back to Kathmandu. Wake up before you get a notice that says you’ve been "re‑educated".

Anjali Govind

May 20, 2025 AT 04:28Totally get where both sides are coming from. While the crackdown seems harsh, many families just can’t afford the bank fees and wait times. A lot of the underground groups actually provide informal insurance – like if a transaction gets flagged, they’ll try to move the funds through a different route. Still, the legal exposure is real, so it’s best to keep amounts low and split them across multiple friends. Also, staying in private Telegram channels rather than public forums can reduce visibility. If you’re new to this, start with small test transfers to see how the system reacts before moving larger sums.

Lady Celeste

May 27, 2025 AT 13:28Crypto drama is just a cheap hype train.

Ethan Chambers

June 3, 2025 AT 22:28Ah, the classic “let's ban everything” playbook – typical of governments that can’t innovate. They love to parade around statutes while the real economy quietly pivots to decentralized solutions. It’s almost poetic, really, that the very act of prohibition fuels a more resilient, underground ecosystem. If they really wanted to help their citizens, they’d embrace blockchain’s transparency instead of criminalizing it. The irony is palpable when they talk about “financial stability” while pushing people to use shady P2P apps that could be even riskier. One could argue this is a perfect case study in regulatory overreach breeding the very thing it fears.

gayle Smith

June 11, 2025 AT 07:28Look, the drama isn’t just about fees; it’s about power dynamics. Those offshore exchanges you’re bragging about? They’re riddled with exit scams. The moment a new regulation hits, the whole chain collapses. You think you’re safe using a VPN, but the moment you download a shady app, your device is a billboard for malware. The more you talk about “hustle”, the more you’re feeding the narrative that this is a wild west, when it’s really a controlled experiment. Tread carefully, and maybe consider the human cost before jumping into the next “revolution”.

Rama Julianto

June 18, 2025 AT 16:28Yo, quick tip for anyone diving into the crypto remittance scene: always double‑check the exchange rates before you lock in a trade. I've seen folks lose $50+ because they relied on a cached price on their phone. Use a reputable rate tracker like CoinGecko or a trusted API. Also, when sending to a friend abroad, ask them to confirm receipt ASAP – that way you can catch any swapped addresses early. For extra safety, mix up your transaction times; don’t always send at 9 am sharp, or you’ll look like a pattern for the watchdogs. And please, never share your private key in any chat – even if someone seems legit.

Helen Fitzgerald

June 26, 2025 AT 01:28Great advice! Adding to that, using a hardware wallet is a game‑changer. It keeps your keys offline, which means even if your phone gets compromised, the funds stay safe. Also, for those using P2P apps, try to find groups with escrow services – it adds a layer of protection against scams. And, if you’re comfortable, consider splitting the transfer into multiple smaller amounts across different days. That way, if something goes sideways, you’re not losing the whole batch. Keep those vibes positive and stay safe out there!

Jon Asher

July 3, 2025 AT 10:28Thinking about using crypto for sending money home? The biggest thing to remember is that the fees on most platforms are hidden until the last step. Make sure you read the fine print, and compare a few different services before you choose one. Also, keep your transactions under the radar by varying the amounts and timing – that helps avoid drawing attention from the authorities. And if you have any doubts, talk to someone in the diaspora who’s already doing it safely. It’s all about sharing knowledge and staying low‑key.

hrishchika Kumar

July 10, 2025 AT 19:28Totally agree, the community aspect is crucial. In my experience, groups on Discord that have a reputation system tend to weed out scammers faster. Also, remember that the NRB can request data from ISPs, so using a reputable VPN service with a no‑logs policy is a must. One more thing – always have a backup of your seed phrase stored offline, maybe in a safe deposit box, because losing that means losing access forever. Thanks for bringing a balanced view, everyone!

Nina Hall

July 18, 2025 AT 04:28Hey folks, just wanted to share a quick win I had. I used a peer‑to‑peer app that lets you escrow the crypto until the recipient confirms receipt. The fee was under 1%, and the transfer showed up in their bank within an hour. It felt great to see the family get the money without the usual 3‑5 day wait. If you haven’t tried an escrow service yet, give it a shot – it adds peace of mind.

Lena Vega

July 25, 2025 AT 13:28Nice tip, thanks!

Laura Myers

August 1, 2025 AT 22:28Okay, let’s get real for a sec. The hype around “crypto freedom” is sold like candy, but the reality in Nepal feels more like a high‑stakes poker game. You’re dealing with a government that has already slapped hefty fines and prison time on anyone caught with a private wallet. The underground scene is fragmented, and trust is a luxury you can’t afford to waste. If you’re thinking of going all‑in, you need a solid contingency plan – multiple wallets, diversified entry points, and an exit strategy that isn’t just “pray it won’t get seized”. It’s not a weekend hobby; it’s basically a covert operation.

Leo McCloskey

August 9, 2025 AT 07:28Well, that’s a very romanticized view of a very dangerous game. The fact remains that any individual engaging in illegal activity cannot expect leniency. The law is clear, the penalties are explicit, and the enforcement mechanisms are getting more sophisticated every day. There’s no silver bullet here – just a cold hard reality that should make you think twice before proceeding.

Sanjay Lago

August 16, 2025 AT 16:28Hey all, just wanted to throw in a positive spin. While the ban is strict, the ingenuity of the diaspora shows that people find ways to stay connected. If you’re new to the scene, start small, learn the ropes, and always keep a backup plan. The upcoming CBDC could actually be a helpful tool if used correctly, offering faster settlements without the legal gray area of private crypto.

arnab nath

August 24, 2025 AT 01:28Sure, but the truth is that every “small step” you take builds a paper trail. The government monitors transaction patterns, and even low‑volume moves can be flagged if they’re consistent. It’s not just about the amount; frequency matters. So be aware that trying to stay under the radar may still land you in hot water if the authorities decide to crack down on the whole network.

Nathan Van Myall

August 31, 2025 AT 10:28When evaluating the viability of cryptocurrency as a solution for Nepalese remittances, it is essential to consider both macro‑economic and micro‑level factors that influence user adoption. Firstly, the cost differential between traditional banking channels and crypto platforms is stark; banks typically levy fees ranging from 5% to 10% of the transfer amount, whereas many crypto services operate on sub‑1% fee structures, dramatically increasing net receipts for recipients. Secondly, transaction speed is a critical component; bank transfers can take anywhere from three to five business days, while blockchain confirmations for popular coins like Bitcoin or Ethereum can be completed within minutes, depending on network congestion. Thirdly, the regulatory environment imposes an additional layer of risk, as the Nepal Rastra Bank's enforcement mechanisms have evolved to include sophisticated blockchain analytics tools capable of deanonymizing users who rely on VPNs and mixers. Fourth, cultural acceptance plays a role; older generations may view crypto with suspicion, but younger migrants in the Gulf or Malaysia often act as intermediaries, introducing the technology to familial networks. Fifth, the security of private keys remains a paramount concern; loss or theft of a seed phrase equates to irreversible loss of assets, a scenario that is exacerbated by low digital literacy in certain communities. Sixth, the upcoming central bank digital currency (CBDC) could potentially mirror the benefits of crypto-speed and lower costs-while providing governmental oversight, thereby creating a hybrid model that may reduce the appeal of private cryptocurrencies. Seventh, liquidity considerations are relevant; converting crypto to fiat in Nepal requires access to local exchanges or peer‑to‑peer platforms, which may suffer from limited depth, leading to slippage. Eighth, the volatility of crypto assets introduces exchange rate risk; while stablecoins mitigate this, they are themselves subject to regulatory scrutiny and may be deemed illegal under current statutes. Ninth, the social cost linked to potential legal repercussions includes not only monetary fines but also imprisonment, which can have a cascading impact on families dependent on remittance income. Tenth, finally, a comprehensive risk‑reward analysis must weigh these variables against personal risk tolerance and the urgency of the remittance need, recognizing that in many cases the marginal gain in speed and reduced fees may be offset by heightened legal exposure and operational complexities.

debby martha

September 7, 2025 AT 19:28Yup, that’s a lot to think about.

Ted Lucas

September 15, 2025 AT 04:28Wow, let’s pump some hype into this conversation! 🚀 Crypto isn’t just a cheap money transfer tool; it’s a revolution that shatters the old‑school banking monopoly. Imagine a world where your cousin in Qatar can zip cash to your mom in Kathmandu faster than the post office, and all without the middle‑men skimming off the top. The tech is robust, the community is fierce, and the risk? Yeah, there’s always risk, but that’s the thrill of being on the cutting edge. Keep those wallets funded, stay sharp on security, and watch the old guard tremble as the new dawn rises. 💥

ചഞ്ചൽ അനസൂയ

September 22, 2025 AT 13:28Appreciate the enthusiasm, but let’s ground it a bit. The spirit of innovation is powerful, yet the reality of enforcement in Nepal is not something to overlook. While the tech can be empowering, the practical steps – such as using multi‑signature wallets, rotating VPN servers, and maintaining an offline backup – are essential to stay safe. It’s a delicate balance between excitement and caution.

Orlando Lucas

September 29, 2025 AT 22:28Stepping back from the hype, I think it’s valuable to view this through a philosophical lens. Money, at its core, is a social contract, a shared belief system that enables exchange. By introducing cryptographic scarcity and decentralization, we’re challenging the very foundations of that contract, questioning the authority of nation‑states over value creation. This tension creates not just economic friction but also cultural evolution, prompting societies to redefine trust. In Nepal’s case, where remittances are a lifeline, the clash is palpable: the state's desire to control capital flows versus the diaspora’s need for efficiency and autonomy. The upcoming CBDC will likely attempt to reconcile this by embedding state oversight into a digital form, perhaps reshaping the contract rather than discarding it. The crucial question remains: will this integration preserve the beneficial aspects of decentralization, such as speed and low cost, or will it merely rebrand the existing centralized mechanisms? The outcome will influence not only financial habits but also the collective perception of sovereignty.

Jacob Moore

October 7, 2025 AT 07:28Great philosophical take! Building on that, a practical tip: if you’re exploring the CBDC once it launches, treat it like any other digital platform – enable two‑factor authentication, keep your phone’s OS updated, and use reputable wallets provided by the central bank. Also, keep an eye on community forums for any quirks or bugs that early adopters discover. Balancing theory with everyday security habits is the sweet spot.

Manas Patil

October 14, 2025 AT 16:28From a cultural standpoint, it’s fascinating how the Nepali diaspora is shaping a new narrative around money. The blend of traditional family obligations with cutting‑edge tech creates a unique hybrid that could serve as a model for other remittance‑heavy economies.

Annie McCullough

October 22, 2025 AT 01:28Sure, but don’t forget that every “new narrative” eventually faces the same old reality – regulations will catch up, and the dream will be monetized. 😏