NRI Crypto Tax Rules 2026: No Exemptions, Just Strict Compliance

May, 12 2026

May, 12 2026

Many Non-Resident Indians (NRIs) assume that their foreign income and investments are shielded from Indian tax laws. For traditional assets like stocks or bonds, this assumption often holds true thanks to specific exemptions under Section 115F. But when it comes to cryptocurrency, the reality is starkly different. If you are an NRI trading digital assets, there are no special tax breaks waiting for you in New Delhi.

In fact, the current regulatory framework treats your crypto gains almost identically to those of a resident taxpayer, with one major twist: the new residency rules taking effect in April 2026 could pull more of your global income into the Indian tax net. This article breaks down exactly how Virtual Digital Assets (VDAs) are taxed for NRIs, why you can't use standard NRI exemptions, and what the upcoming changes mean for your wallet.

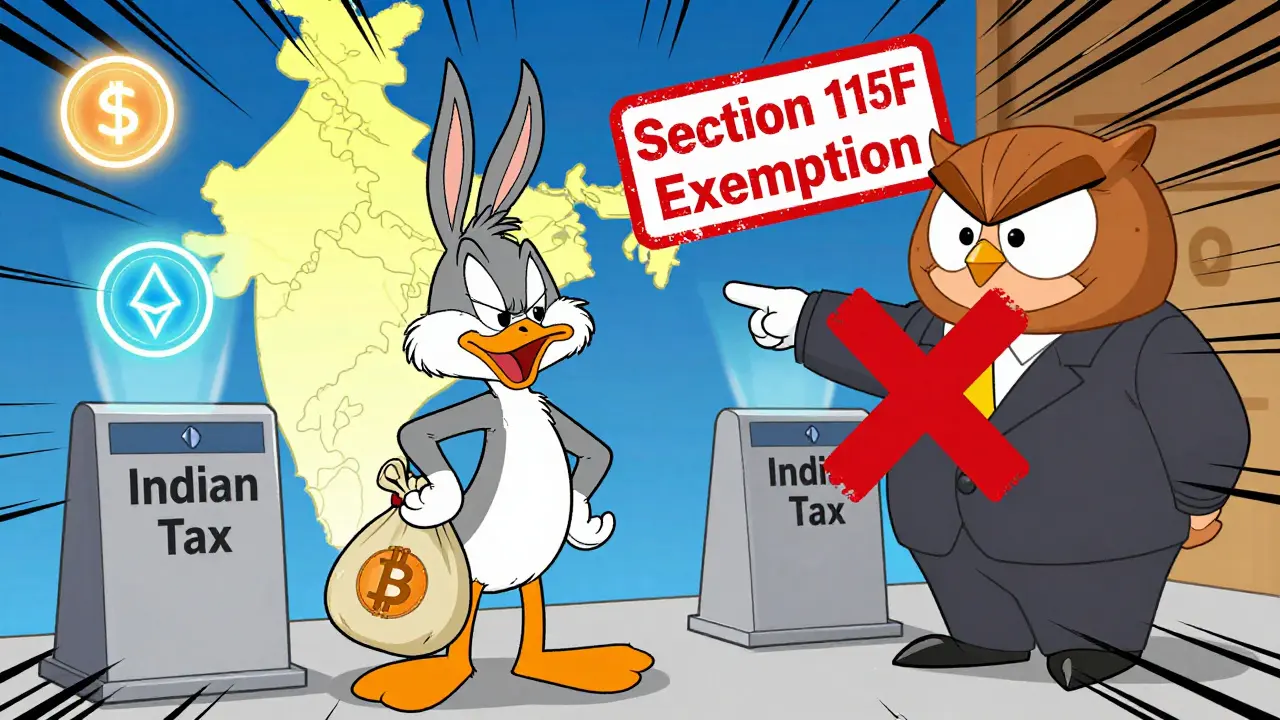

The Hard Truth: No Special Exemptions for NRI Crypto Investors

Let’s clear up the biggest misconception first. Under Indian tax law, NRIs enjoy certain benefits when they reinvest proceeds from specific financial instruments. For example, if you sell shares of an Indian company, you might avoid capital gains tax by reinvesting in approved mutual funds or bonds. This is governed by Section 115F of the Income Tax Act.

Cryptocurrency does not qualify for this treatment. The government explicitly excludes VDAs from the list of eligible assets for these exemptions. Whether you hold Bitcoin, Ethereum, or any of the 1,500+ other recognized tokens, your gains are subject to the standard VDA tax regime. There is no 'NRI discount' on crypto taxes.

- No Long-Term Capital Gains Benefit: Unlike stocks, where holding an asset for over a year reduces your tax rate, crypto gains are taxed at a flat 30% regardless of how long you held them.

- No Loss Offsetting: You cannot offset losses from one crypto trade against profits from another. Furthermore, you cannot deduct crypto losses from your salary or business income.

- Limited Deductions: When calculating your taxable gain, you can only deduct the purchase price of the asset. Transaction fees, gas costs, storage fees, and software subscriptions are not deductible expenses.

This uniform approach means that an NRI living in Dubai faces the same 30% tax liability on Indian-sourced crypto gains as a resident living in Mumbai. The lack of differentiation creates a challenging environment for non-residents who rely on tax efficiency in other asset classes.

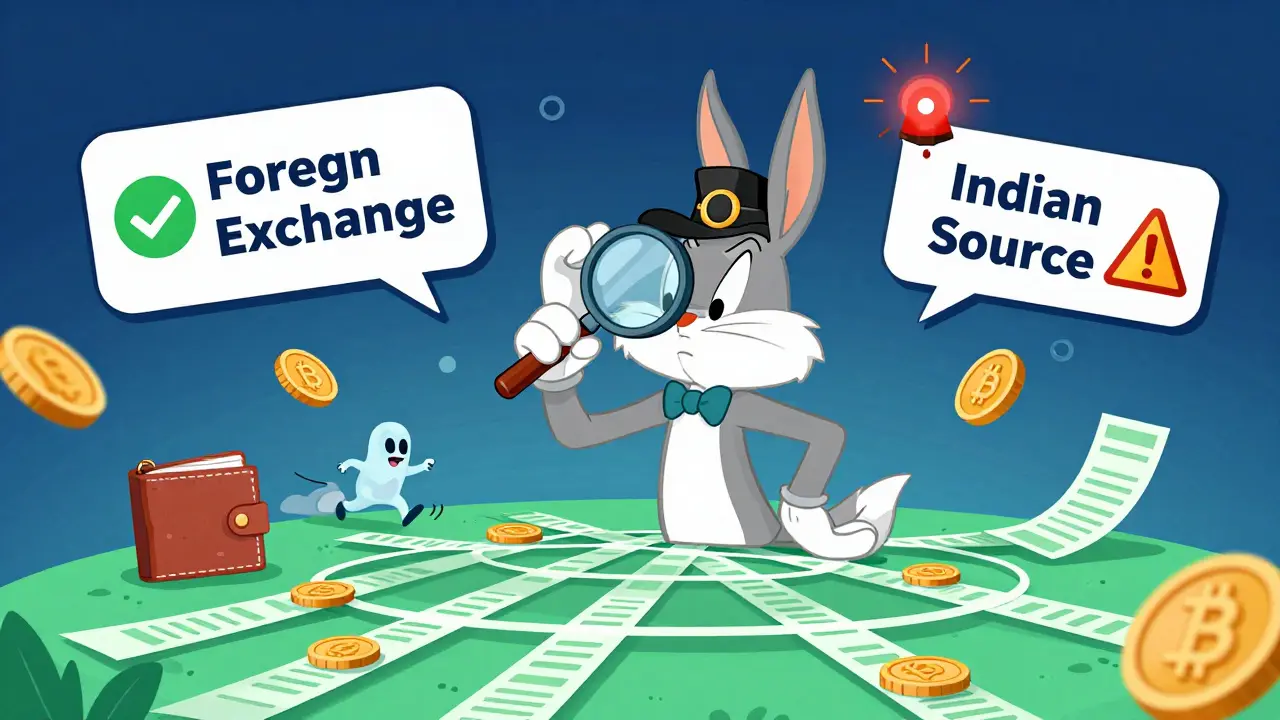

How Your Residency Status Defines Your Tax Liability

Your tax obligation in India depends entirely on your residency status. For NRIs, the rule is straightforward: you are generally taxed only on income earned or received within India. However, defining what constitutes "Indian source" income for cryptocurrency is tricky and often ambiguous.

If you buy Bitcoin on a US-based exchange and sell it while living in Singapore, Indian tax authorities typically view this as foreign-source income, which is not taxable in India. But if you use an Indian exchange, or if the transaction involves Indian counterparties, the income may be deemed Indian-sourced. The Resident but Not Ordinarily Resident (RNOR) category adds another layer of complexity. Many NRIs fall into this bucket during transition years. RNORs are taxed only on income earned or received in India, excluding foreign income unless it is derived from a business controlled in India.

Here is where things get dangerous for many investors. The definition of "received in India" can include crypto sent to an Indian bank account or wallet address linked to an Indian entity. Without meticulous record-keeping, you risk being classified as having Indian-source income, triggering the 30% tax plus penalties.

The 2026 Residency Rule Change: A Major Shift

Pay close attention to this update. Starting April 1, 2026, the threshold for becoming a tax resident in India drops significantly. Previously, staying in India for 182 days or more made you a resident. The new rule lowers this to 120 days, provided your income from Indian sources exceeds ₹15 lakhs (approximately $18,000 USD).

For NRIs who travel frequently to India for family visits, business meetings, or property management, this change is critical. If you cross the 120-day mark and meet the income threshold, you become a tax resident for that financial year. As a resident, your global income becomes taxable in India. This includes all your cryptocurrency gains, whether traded on Binance, Coinbase, or decentralized platforms abroad.

This shift effectively eliminates the "NRI shield" for many high-net-worth individuals. You must now track your physical presence in India with greater precision. A single extended holiday combined with freelance crypto earnings could push you into residential status, exposing your entire global portfolio to Indian taxation.

Tax Deducted at Source (TDS): The Hidden Cost

Even if you plan to pay your taxes later, the immediate friction comes from Tax Deducted at Source (TDS) under Section 194S. This mechanism requires Indian exchanges and brokers to withhold 1% of the sale value at the time of transaction.

For NRIs using Indian platforms, this deduction happens automatically. If you sell ₹10 lakh worth of crypto, ₹10,000 is withheld immediately. While this amount is creditable against your final tax liability, it impacts your cash flow. More importantly, recent clarifications suggest that even smaller transactions-sometimes as low as ₹10,000-may trigger reporting requirements, increasing compliance burdens.

If you trade exclusively on foreign exchanges, TDS under Section 194S does not apply directly. However, you still have a self-assessment liability. You must declare these gains in your Indian income tax return if they are deemed Indian-source income. Failure to disclose can lead to scrutiny under the Foreign Exchange Management Act (FEMA) and potential blacklisting.

Special Cases: Mining, Airdrops, and Gifts

Not all crypto acquisitions involve buying and selling. What about rewards? If you receive cryptocurrency through mining, staking rewards, airdrops, or gifts, the tax treatment differs slightly-but not in your favor.

These receipts are treated as "income from other sources" rather than capital gains. They are taxed at your applicable slab rate. For an NRI with significant other income, this could mean a higher effective tax rate than the flat 30% applied to sales. Additionally, when you eventually sell these gifted or mined coins, the cost basis is zero (or fair market value at receipt), meaning the entire future sale price is taxable as a gain.

Example: You receive 1 ETH as an airdrop. Its value is ₹200,000. You pay tax on ₹200,000 at your slab rate. Later, you sell it for ₹300,000. You pay 30% tax on the ₹100,000 profit. You’ve been taxed twice on the same asset.

Practical Steps for NRI Crypto Compliance

Navigating this landscape requires discipline. Here is a checklist to keep you compliant and minimize risks:

- Maintain Detailed Records: Keep logs of every transaction, including date, time, amount, fiat equivalent at the time, and platform used. Screenshots alone are insufficient; use exportable CSV files from exchanges.

- Track Physical Presence: Use a calendar app to monitor your days in India. Aim to stay below 120 days if you wish to maintain NRI status post-2026.

- Segregate Wallets: Consider using separate wallets for Indian-sourced activities versus foreign-sourced ones to simplify tracking and reporting.

- Consult a CA Familiar with VDAs: General chartered accountants may not understand the nuances of crypto taxation. Seek specialists who follow updates from the Income Tax Department regarding Virtual Digital Assets.

- Review Double Taxation Avoidance Agreements (DTAA): Check if your country of residence has a DTAA with India. While crypto isn’t always covered, some agreements allow credits for taxes paid abroad, preventing double taxation.

The goal is not to evade tax, but to ensure accurate reporting. The Indian tax authority has increased its focus on digital assets, leveraging data sharing with global exchanges. Proactive compliance protects you from audits and penalties.

Do NRIs pay tax on crypto gains earned outside India?

Generally, no. NRIs are taxed only on income earned or received in India. If you buy and sell crypto on foreign platforms while residing abroad, those gains are typically not taxable in India. However, if the income is received in an Indian bank account or wallet, it may be considered Indian-source income.

Can NRIs claim the Section 115F exemption for crypto investments?

No. Section 115F exemptions apply to specific financial instruments like bonds, debentures, and mutual funds. Cryptocurrency and other Virtual Digital Assets are explicitly excluded from these benefits.

What is the tax rate for NRI crypto sales in India?

The tax rate is a flat 30% on capital gains, plus a 4% health and education cess. There is no distinction between short-term and long-term holdings, and no deductions are allowed except for the purchase cost.

How does the 120-day rule affect NRIs in 2026?

Starting April 1, 2026, staying in India for 120 days or more (with Indian income over ₹15 lakhs) makes you a tax resident. As a resident, your global crypto gains become taxable in India, removing the NRI protection for foreign-sourced income.

Is TDS applicable to NRIs trading on Indian exchanges?

Yes. Under Section 194S, Indian exchanges must deduct 1% TDS on crypto transactions exceeding specified thresholds. This applies equally to residents and NRIs.